Background of Equalisation Levy

Today the world has narrowed down and geographical boundaries have remained on paper only. Digitization of business has changed traditional methods and has provided ease of doing business. And there is always some cost to be paid for availing the ease. And we can say equalization levy is that small cost.

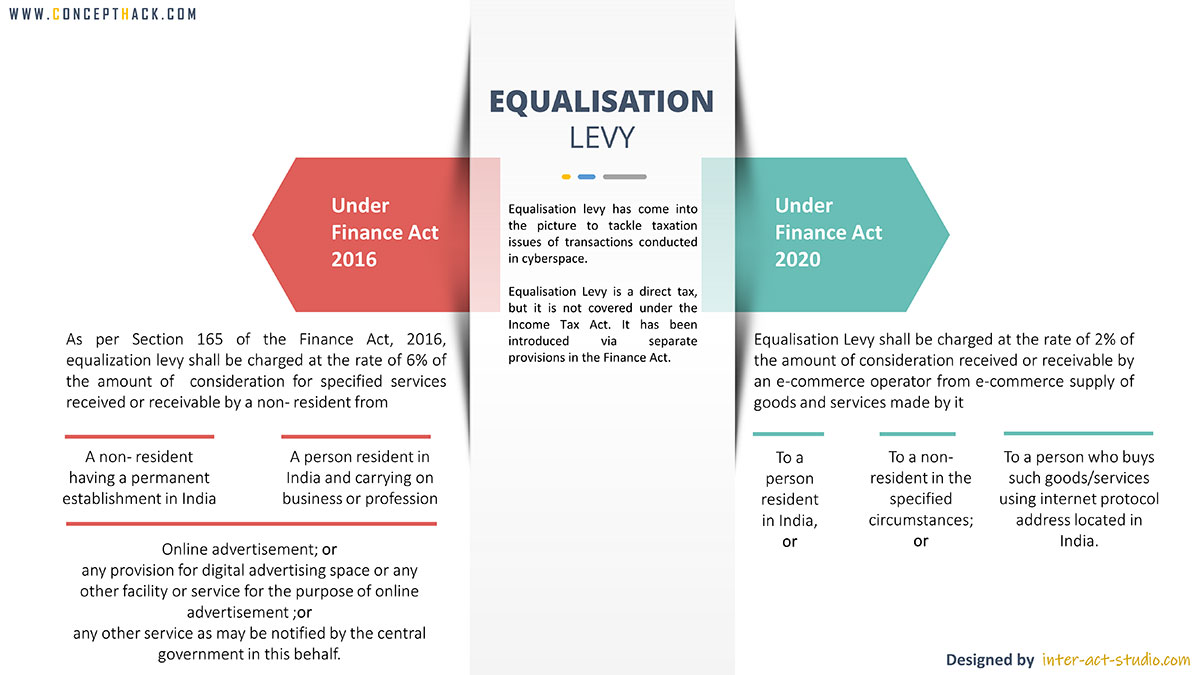

Equalisation levy has come into the picture to tackle taxation issues of transactions conducted in cyberspace.

Equalisation Levy is a direct tax but it is not covered under the Income Tax Act. It has been introduced via separate provisions in the Finance Act.

Significance of Equalisation Levy

Since the last few years, Information Technology has shown vital growth in India and around the world. This has led to rise in the demand and supply of digital services. As a result, various new types of businesses have emerged which are mainly conducted through digital and telecommunication networks. And that has raised challenges to set up the environment to bring such transactions under the tax bracket. To resolve issues arising out of such transactions, the government introduced vide Budget 2016, the equalisation levy and subsequently it was amended vide Budget 2020 to widen the scope of equalisation levy.

Equalisation Levy under Finance Act 2016

When Equalisation Levy is not applicable?

- The non-resident providing specified service has a permanent establishment in India and income from such specified service is effectively connected to this permanent establishment; or

- Where the specified service is not for the purpose of carrying out business or profession; or

- The aggregate amount of consideration payable for the specified service received or receivable does not exceed Rs. 1 lakh in any previous year.

Let us understand the concept based on examples:

Example 1: Mr.A has availed services of Google for promotion of clothes business and advertises his products on and has made a payment of Rs. 1,50,000/- to Google for the advertising services availed.

Solution: As per the provisions of Sec.165 of Finance Act, Mr. A is liable to deduct equalisation levy @6% from payment of Rs. 1,50,000/- i.e. Rs. 9,000/-shall be deducted and deposited as equalisation levy and Google will get balance payment of Rs. 1,41,000/-.

Example 2: Ms. H has availed advertisement services of Facebook for her personal purpose. She has paid Rs. 1,10,000/- for the same.

Solution: According to the exemption list, Ms. H is not liable to deduct an equalisation levy because she has not used services for carrying out business or profession.

Example 3: Mr. D has advertising services of Facebook for promoting his business and paid Rs. 90,000/- for availing the services.

Solution: According to the chargeability section, as payment made by Mr. D does not exceed Rs. 1,00,000/- , he is not liable to deduct equalisation levy.

What is the Collection & recovery procedure of Equalisation Levy?

The amount of equalisation levy so deducted by the payer has to be paid to the credit of the government of India by 7th day of the month following the month in which the equalisation levy is deducted.

Even if equalisation levy is not deducted, the payer is liable to pay the levy to the credit of the central government.

Let us understand by way of example:

Example: Mr. A has deducted equalisation levy of Rs. 9000/-on 10th January 2018 then in this case he is supposed to deposit the same with central government on or before 7th February 2018.

What is the Due Date of Furnishing the statement?

Due date of furnishing equalisation levy statement (in Form No. 1) is on or before 30th June of Financial Year immediately following the financial year in which equalisation levy is chargeable. This is the annual statement.

Example: Mr. A has deducted and deposited equalisation levy during the year 2017-2018 then he has to submit the statement in Form No.1 by 30th June 2018.

What is the Interest on delayed payment?

Simple interest is charged at 1% on the outstanding levy for every month or part of the month during which such failure continues. (Section 170 of the Finance Act 2016)

Let us understand by way of example.

Example: Mr. A has deducted equalisation levy of Rs. 9,000/-on 10th January 2018 and deposited the same on 15th May 2018 then he is supposed to pay Interest for 5 months (From January to May) at 1% per month on Rs. 9,000/- and it will amount to Rs. 450/-(9000*1%*5).

What is the Penalty in case of non-compliance?

| Situation | Penalty (in addition to paying equalisation levy and interest) | Example |

|---|---|---|

| Failure to deduct equalisation levy (wholly or partly) | A penalty equal to amount of equalisation levy |

|

| Failure to deposit with government | Rs. 1000 for each day of default (not to exceed amount of equalisation levy) |

|

| Failure to furnish statement | Rs. 100 for each day of default | Mr. A fails to furnish the statement by 30th June 2018 [for FY 2017-18] and delayed it by 15 days so penalty will be Rs. 1500/- (Rs. 100/day*15 days). |

Exemption from Income Tax

When equalisation levy is deducted under the above provisions, income of the recipient non- resident is exempt under section 10(50).

** Section 10(50):-

Section 10(50) provides that any Income arising from any specified service provided on or after the date on which provisions of Chapter VIII of the Finance Act,2016 comes into force shall not form part of Total Income.

Equalisation Levy under Finance Act 2020

What is meant by E-Commerce Operator?

It means a non- resident who owns, operates or manages a digital or electronic facility or platform for online sale of goods or online provision of services or both.

What is the meaning of Online Supply or Services?

- Online sale of goods owned by the e commerce operator; or

- Online provision of services provided by the e commerce operator; or

- Online sale of goods or provision of services facilitated by the e commerce operator; or

- Any combination of the above activities

What is the meaning of specified circumstances?

- Sale of advertisement, which targets a customer, who is resident in India or a customer who access the advertisement through internet protocol address located in India; and

- Sale of data collected from a person who is resident in India or from a person who uses internet protocol address located in India

When Equalisation Levy is not applicable?

- E- commerce operator has a permanent establishment in India and such e commerce supply is effectively conducted with such permanent establishment;

- Equalisation levy is levied under the provisions given under section 165 of the Finance Act, 2016; or

- Sales, turnover or gross receipts, of the e-commerce operator from the e-commerce supply or services made or provided or facilitated is less than Rs. 2 crore during the previous year.

Let us understand the concept based on some examples:

Example: Amazon receives a consideration of Rs. 50 crores towards the e-commerce supply of goods and services in its Indian marketplace amazon.com, (we are assuming that amazon.com does not have permanent establishment in India), to Indian Residents during the previous year 2020-21. Thus, by virtue of the newly inserted section 165A of the Finance Act,2020 Amazon shall be required to deposit an equalisation levy @ 2% on its total turnover of Rs. 50 crores from the e-commerce supply of goods and services to the Indian Residents, i.e. Rs. 1 crores with the Exchequer in India.

What is the collection & recovery procedure of Equalisation Levy?

The equalisation levy shall be paid by every e-commerce operator to the credit of government quarterly within the following due dates:

| Date of ending of quarter | Due Date | Example |

|---|---|---|

| 30 June | 7 July | Liability of Mr. A of equalisation levy for the quarter April-June’2020 is Rs. 9000/- then he is supposed to deposit the same with the central government by 7th July 2020. |

| 30 September | 7 October | Liability of Mr. A of equalisation levy for the quarter July-September’2020 is Rs. 10,000/- then he is supposed to deposit the same with the central government by 7th October 2020. |

| 31 December | 7 January | Liability of Mr. A of equalisation levy for the quarter October-December’2020 is Rs. 12,000/- then he is supposed to deposit the same with the central government by 7th January 2021. |

| 31 March | 31 March | Liability of Mr. A of equalisation levy for the quarter January-March’2021 is Rs. 15,000/-then he is supposed to deposit the same with the central government by 31st March,2021. |

What is the Due Date of furnishing the statement?

Every e-commerce operator shall furnish a statement electronically within a specified time in a specified form in respect of e-commerce supply of goods or services during the financial year.

Example: Mr. A has deducted and deposited equalisation levy during the year 2020-2021 then he has to submit the statement in Form No.1 by 30th June 2021.

What is the Interest on delayed payment?

Simple interest is charged at 1% on the outstanding levy for every month or part of the month during which such failure continues

Let us understand by way of example.

Example: Mr. A has deducted equalisation levy of Rs. 9,000/-on 10th January 2021 and deposited the same on 15th May 2021 then he is supposed to pay Interest for 5 months (From January to May) at 1% per month on Rs. 9,000/- and it will amount to Rs. 450/-(9000*1%*5).

What is the Penalty in case of non-compliance?

| Situation | Penalty (in addition to paying equalisation levy and interest) | Example |

|---|---|---|

| Failure to deduct equalisation levy (wholly or partly) | A penalty equal to amount of equalisation levy |

|

| Failure to furnish statement | Rs. 100 for each day of default | Mr. A fails to furnish the statement by 30th June 2021 [for FY 2020-21] and delayed it by 15 days so penalty will be Rs. 1500/- (100Rs/day*15days). |

Exemption from Income Tax

Income from the above activities in the hands of e-commerce operators is exempt under section 10(50) with effect from the assessment year 2021-22.

** Section 10(50):-

Section 10(50) provides that any Income arising from any specified service provided on or after the date on which provisions of Chapter VIII of the Finance Act, 2016 comes into force shall not form part of Total Income. The Finance Act 2020 substitutes the words Comes into force or arising from any E-Commerce Supply or services made or provided or facilitated on or after the 1st day of April,2021 for the words ‘comes into force’.

How to make payment of Equalisation Levy (Finance Act 2016 &2020)?

In order to enable the payment of equalisation levy, the CBDT has amended the existing payment challan (viz, ITNS 285) so as to permit the use of the same challan for payment of equalisation levy as applicable for non-resident e-commerce operators and for the deductor of specified services. It is important to note that the challan mandatorily requires the non-resident e-commerce operators to also quote their Permanent Account Number (‘PAN’) before making the payment. It may be noted that the mandate to obtain a PAN in India is procedural in nature despite there being no statutory requirement.

{kind=link}