Background

Income tax is a direct tax and it has set traditional rules and procedures for various provisions. But now time is changing and digitization has taken place in many fields. The traditional assessment procedure has certain major issues which used to occur mainly due to human intervention. Assesses have to face harassment from the department officials. Central government has introduced a faceless assessment scheme to provide major transparency, efficiency and accountability in Income tax assessments. It will make both department and assessee responsible for their roles and will save time also.

We will discuss important points under the following heads.

I will cover the following points to explain the topic.

What is a faceless income tax assessment? When was it introduced?

The scheme was launched on 7th October 2019. The scheme was introduced to eliminate the human interface between the taxpayer and the income tax department. The scheme lays down the procedure to carry out a faceless assessment through electronic mode. From 13th August 2020, the e-assessment scheme of 2019 stands amended and hence known as the Faceless Assessment scheme. Initially the faceless assessment scheme applied only to scrutiny assessment and best judgment assessment. However, as per the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Bill, 2020, Faceless Assessment will now cover other provisions of the Income Tax Act, 1961 under its purview.

The e-assessment would be made in respect to such territorial area, or persons or class of persons, or income or class of income, or cases or class of cases, as may be specified by the Central Board of Direct Taxes (CBDT).

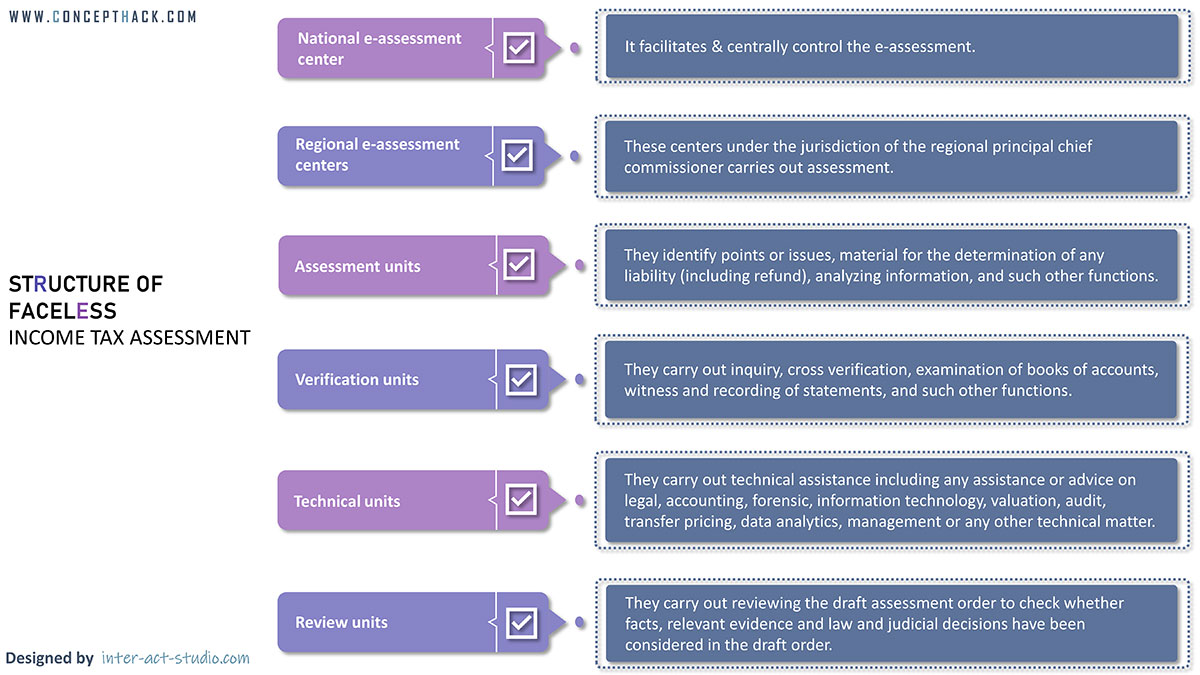

What is the structure of faceless assessment?

What is the procedure of faceless assessment?

The procedure of e-assessment is as below:

Step 1: National e-assessment center will issue notice under section 143(2) specifying issues for selection of taxpayer’s case for assessment

Step 2: The taxpayer has to file response with National e-assessment center within 15 days

Step 3: The National E-Assessment Centre will assign the case selected for the purposes of e-assessment to a specific ‘assessment unit’ in any one ‘Regional e-Assessment Centre’ through an automated allocation system.

Step 4: Once a case is assigned to an assessment unit, it may make a request to the National e-Assessment Centre for:

- Acquiring such further information, documents, evidence from the taxpayer or any other person as specified

- Asking for verification by verification unit

- Seeking technical assistance from the technical unit

Step 5: The National E-Assessment center will in turn ask taxpayers or any other person to provide requested data, documents or evidence to the assessment unit

Step 6: The taxpayer or any designated person needs to submit the response within specified time

Step 7: On receipt of request for verification from the assessment unit, the national e-assessment center will assign the verification request to the verification unit through an automatic allocation system

Step 8: On receipt of request for technical assistance from the assessment unit, the national e-assessment center will assign the technical unit through an automatic allocation system for providing technical guidance

Step 9: The National e-assessment center in turn will send the details received from verification unit or technical unit to the concerned assessment unit

Step 10: If a taxpayer fails to file response to the notice, the national e-assessment center will issue a notice under section 144 for best judgement assessment

Step 11: The taxpayer can file response to the notice issued under section 144.and if he doesn’t send any response then National e-assessment unit will inform the assessment unit to prepare draft assessment order under best judgement assessment (section 144)

Step 12: The assessment unit after considering all the relevant facts, pass a draft assessment order either as per returned income or altering the returned income of the taxpayer and send a copy of the order to the National e-assessment Centre

Step 13: The assessment unit while passing draft assessment order should provide details of penalty proceedings to be initiated therein, if any

Step 14: The National e-Assessment Centre shall examine the draft assessment order and it may decide to

- Finalize the assessment as per draft assessment order and serve the copy of the order along with notice for initiating penalty proceedings, if any and also serve demand notice mentioning sum payable or refund of any amount due to the tax payer, OR

- Provide an opportunity to the tax payer in case of any changes are proposed by serving a notice calling upon him to explain as to why the assessment should not be completed as per the draft assessment order, OR

- Delegate the draft assessment order to any of review unit to carry out review of the order

Step 15: The review unit will carry out review of the draft assessment order and

- May accept the draft assessment order and intimate about its acceptance to the National e-Assessment Centre, OR

- May suggest necessary modifications to the draft assessment order and inform about the modifications to the National e-Assessment Centre

Step 16: The National e-Assessment Centre, upon receipt of acceptance of order from the review unit shall finalize the draft assessment order.

Step 17: In case the review unit has suggested some modification then the National e-Assessment Centre will assign the case to the assessment unit (assessment unit will be different from the unit who has passed draft order) based on an automated allocation system.

Step 18: The assessment unit after considering all the proposed modifications will prepare the final order and will intimate the National e-Assessment Centre.

Step 19: On receipt of final draft assessment order, National e-Assessment Centre will finalize the draft assessment order or will give opportunity to the taxpayer in case any modification is suggested.

Step 20: The taxpayer should file his response with National e-Assessment Centre against the notice issued to him for submission of required details against draft assessment order within specified time

Step 21: The National e-Assessment Centre should

- finalize the assessment order based on draft assessment order if response from the taxpayer is not received ,OR

- Submit the response received from the taxpayer to the assessment unit

Step 22: The assessment unit on receipt of response from the taxpayer will make revised draft assessment order and will intimate the same to National e-Assessment Centre

Step 23: The National e-Assessment Centre on receipt of revised draft assessment order,

- In case no modification against the interest of the taxpayer is proposed with reference to the draft assessment order, finalise the draft assessment; OR

- In case a modification against the interest of the assessee is proposed with reference to the draft assessment order, provide an opportunity to the taxpayer for hearing and making submissions

Step 24: The response furnished by the taxpayer shall be dealt with by the National e-Assessment Centre and the draft assessment order will be finalized.

Can a taxpayer approach a dispute resolution pane? How will the assessment be finalized in that case?

- An eligible tax payer can approach the Dispute Resolution Panel and file his objection with them. In that case Dispute Resolution Panel will give guidelines to the National e-Assessment Centre which in turn forward such suggestions to the assessment unit

- The assessment unit shall prepare a draft assessment order in conformity of the directions issued by the Dispute Resolution panel and send a copy of order to the National Faceless Assessment Centre.

- The National Faceless Assessment Centre shall finalize draft assessment order received from assessment unit and serve a copy of order and notice for initiating penalty proceedings, if any, to the assessee. It shall issue a demand notice, specifying the sum payable by, or refund of any amount due to the assessee on the basis of such assessment.

What is the penalty procedure under the faceless assessment scheme?

- In the course of assessment procedure, if any unit finds that taxpayer or any other concerned person is not complying with the notice, direction or order issued under this scheme then the unit can recommend to the National e-Assessment Centre to initiate penalty proceedings under income tax act.

- On receipt of recommendations, the National e-Assessment Centre will serve a notice to the taxpayer or concerned person calling upon him to justify why penalty proceedings should not be carried out against him.

- The response received from the taxpayer will be sent by the National e-Assessment Centre to the concerned unit who has recommended penalty proceedings.

- The concerned unit based on response received from tax payer,

- Make a draft order of penalty and send the copy of the same to National e-Assessment Centre, OR

- Drop the penalty proceeding after recording reasons for the same and intimate the same to National e-Assessment Centre

- The National e-Assessment Centre shall levy the penalty as per the said draft order of penalty and serve a copy of the same along with a notice for demand on the taxpayer or any other person, as the case may be, and also transfer the records of penalty proceedings to the jurisdictional assessing officer for further action.

Can a taxpayer file an appeal and what is the procedure for the same?

Yes, a taxpayer can file an appeal. An appeal against an assessment order or penalty order made by the National e-Assessment Centre under this scheme can be filed before the Commissioner (Appeals) having jurisdiction over the jurisdictional Assessing Officer.

How the communication takes place between taxpayer and the authority under the faceless assessment scheme?

- All communications between the National e-Assessment Centre and the taxpayer, or his authorized representative, shall be exchanged exclusively by electronic mode.

- All internal communications between the National e-Assessment Centre, Regional e-Assessment Centre and various units shall be exchanged exclusively by electronic mode.

How is the communication between the taxpayer and the authority authenticated?

All the electronic records issued under the scheme shall be authenticated by the National e-Assessment Centre by affixing digital signature or by the taxpayer or any other person by affixing their digital signature or through an EVC (Electronic verification code).

How will communication be delivered between the taxpayer and the authority?

Every notice or order or any other electronic communication under this scheme shall be delivered to the taxpayer, by way of:

- Placing an authenticated copy of the communication in the taxpayer’s Registered account or Sending an authenticated copy thereof to the registered email address of the taxpayer or his authorized representative.

- Uploading an authenticated copy on the assessee’s Mobile App; and followed by a real-time alert to the taxpayer.

- The taxpayer shall file his response to any notice or order or any other electronic communication, under this scheme, through his registered account, and once an acknowledgement is sent by the National e-Assessment Centre containing the hash result generated upon successful submission of response, the response shall be deemed to be authenticated.

Does a taxpayer require appearing before any authority personally?

A taxpayer is not required to appear either personally or through an authorized representative before any unit or Centre under this faceless assessment scheme.

In case a taxpayer or his authorized representative requests for personal hearing or oral submission with respect to assessment proceedings then the department will conduct video conferencing or video telephony as per the guidelines of CBDT.

An income tax authority has the power to examine a taxpayer or record the statement of any taxpayer under this scheme. The income tax authority would do the same through video conferencing or video telephony.

What are the benefits of Faceless assessment scheme?

This scheme has drastically changed traditional methods of assessment procedure. Let us discuss some major advantages of the scheme:

- It has removed human intervention from the entire procedure thereby it has reduced personal prejudices and preferences between taxpayers and authorities.

- It has reduced harassment which a taxpayer has to face in terms of odd timings of appearance before the authorities, delay in work getting done etc.

- One of the major benefits of the scheme is transparency. Earlier it was difficult to maintain transparency due to human touch. But now as everything is online, it becomes easy to maintain track of every step.

- It becomes possible to meet deadlines as everything is on record. It becomes easy to identify the person at fault.

- Persons involved in the entire procedure- both department and taxpayer becomes more aware about their responsibilities and will be alert about their actions.

{kind=link}